Indonesia’s Fintech Inflection Point — Why the Next Decade Will Be Different

A quick glance at my iPhone reveals exactly 30 financial apps, though I’ve used two to three times that many over the years. This comes from both relocating between countries — each requiring its own local fintech stack — and the “occupational hazard” of being a VC, where I sometimes test products before they become mainstream (if they ever do).

As a VC based in Indonesia, I’ve watched fintech evolve from novelty to necessity. Over the past decade, we’ve gone from clunky mobile banking apps to sleek platforms for investments, payments, lending, and insurance. During the pandemic, adoption skyrocketed, driven by retail trading apps, e-wallets, and P2P lending. In Jakarta today, I can leave my wallet at home and still navigate most of my financial life through a smartphone.

But despite this progress, I still rely on a trusty spreadsheet to manage my finances — a quiet reminder that for all the innovation, something’s still missing.

And that’s why I believe we’re at an inflection point in Indonesia’s fintech journey. Not just in terms of market size or digital adoption, but in terms of what users need — and what they now expect. Growth is slowing. Trust is eroding. The “wow” factor of shiny new features is giving way to demand for reliability and long-term value.

One way to understand this shift is by looking at a sector where fintech has dramatically lowered barriers — but not yet delivered widespread engagement: retail equity investing. The surge of new capital market accounts in Indonesia tells us that access has improved. But participation and trust remain fragile.

To make sense of how the evolution of retail investing reflects broader changes in Indonesia’s fintech sector, I turn to the Market.iO framework, starting with the foundational question: how wide is the river we’re navigating?

WIDE River: The Illusion of Scale in Retail Investing

Indonesia’s investment landscape can be characterized as a WIDE-MANY-SLOW market — large in potential, crowded with players, but still lagging in meaningful engagement. With around $800 billion market cap and a growing base of retail investors, the structural foundations are there.

Limited Retail Participation in Capital Markets

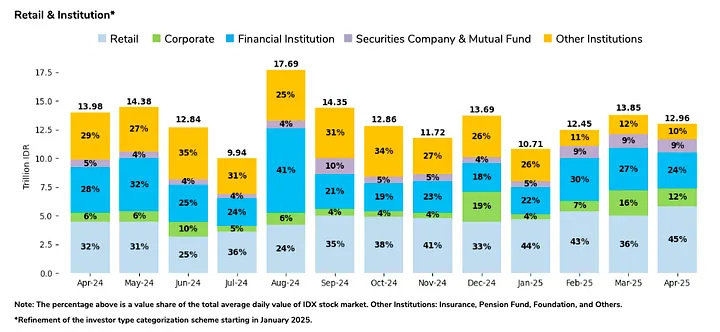

Between 2019 and January 2025, the number of capital market investors jumped from 2.48 million to 15 million, yet less than half contribute meaningfully to trading volume. This gap highlights the disconnect between account creation and actual financial engagement.

During the pandemic, platforms like Ajaib and Bibit helped onboard new investors by simplifying UX and broadening access to products like mutual funds and government bonds. But onboarding alone doesn’t ensure continuing participation.

A rising tide lifts all boats — but fintechs must also prepare for low tides. Sustainable retail investment requires not just accessibility, but education, transparency, and trust.

Fintech companies have made some progress:

- Simplifying financial concepts through content marketing.

- Improving access to low-risk products that were once offline-only.

- Offering more intuitive and mobile-first user interfaces.

But deep engagement will only come when fintechs go beyond UI — toward models that build lasting trust and user confidence.

Persistent Challenges

- Trust Deficit: Disappointing IPOs, lack of a functioning dispute resolution system for retail investors, and misinformation have made investors skeptical.

- Financial Literacy: From miracle investment schemes to exaggerated tales of fraud, this content spreads faster than education can catch up. Many users hesitate not due to disinterest but fear — of scams, losses, or making the wrong choice.

- Access Gaps: In smaller cities and rural areas, financial services are still hard to reach.

Why Now Marks an Inflection Point

- Shifting away from the Awareness Phase: Millions of Indonesians now know how to use digital financial products. But mere access is no longer enough the bar is rising for trust, service quality, and impact.

- Behavior Is Evolving: Users are more cautious. They’re asking harder questions, reading the fine print, and demanding transparency from providers.

- Better Digital Infrastructure: The groundwork laid over the last decade (QRIS, digital KYC, mobile-first design) means fintechs can now build more tailored, secure, and scalable experiences.

What’s Different Going Forward

Until now, fintechs succeeded by building for access. But the next decade will be defined by building for outcomes.

- From Distribution to Depth: The next wave will focus on improving outcomes, not just onboarding new users.

- From Product-Led to Trust-Led Growth: Building brand reliability and dispute resolution channels will matter more than flashy UIs.

- From One-Size-Fits-All to Segmented Solutions: Fintechs will need to meet users where they are — by offering more relevant and contextual products.

The tools and infrastructure are in place. The mindset shift — one that values sustainability over scale, trust over speed, and long-term value over short-term wins — is just beginning.